Accounting Tech Stack: Build the Right System for Scaling Your Firm

Updated February 9, 2026 with new data.

In many settings, the role of an accountant has evolved from number crunching to strategic advising. To meet these new responsibilities, the right accounting tech stack is more important than ever before. A carefully curated tech stack helps businesses stay compliant, simplify workflows, scale sensibly, and provide more value to their clients.

It also plays an active role in mitigating risk, enabling real-time reporting, and helping accounting firms better serve their clients through data-informed decision-making.

But with so many tools available, how do you decide what to include and how to optimize it?

Let's explore the components of a robust tech stack for accounting firms, as well as how to evaluate tools and best practices for making the most of your investment.

For firms new to tech adoption, it’s often best to start small. Rather than implementing a dozen tools at once, choose one or two high-impact platforms and build from there. This allows teams to gradually adjust and avoids overwhelming staff with too many changes simultaneously.

What Is an Accounting Tech Stack?

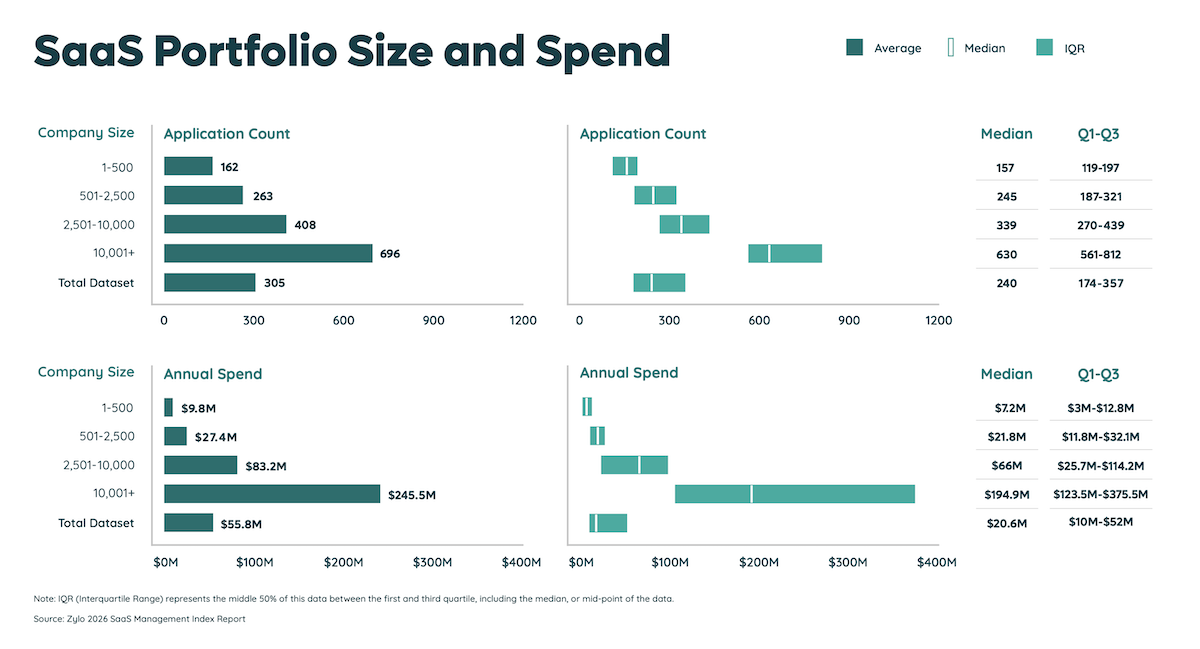

An accounting tech stack is the collection of software programs an accounting firm uses to manage operations, client services, and internal workflows. This includes everything from key accounting software to automation, security, time tracking, HR, and tax planning. It can also include specialized analytical tools, CRM platforms, and document management solutions, depending on the firm's scope and services. The size of your accounting tech stack depends on the size of your firm, and our data shows that the average company has 305 applications.

Each tool in the stack should serve a specific purpose and integrate seamlessly with programs already in the stack. When every corner is covered, these platforms streamline daily tasks, reduce human errors, ensure strict compliance, and help the firm grow. A well-structured tech stack both enhances operational efficiency and improves employee satisfaction by removing much of the friction from daily tasks.

Integration is especially important. Even the best individual tools lose value if they can’t interact with others in the stack. When evaluating new platforms, always consider compatibility with your existing systems, especially around data import/export, login systems, and real-time syncing.

Why Businesses Need an Accounting Tech Stack

Accounting firms are facing mounting pressure to achieve more with fewer resources available. This could take the form of fewer staff members, tighter deadlines, and growing client expectations. A strong tech stack addresses these challenges preemptively by automating manual tasks, reducing costs, and presenting greater transparency throughout the firm.

The benefits of having an adequate tech stack include:

Compliance

Regulatory requirements are constantly changing. With the right tech stack, accounting firms can automate tax filings, maintain data security, and stay ahead of industry changes. Some compliance platforms also include built-in audit trails and e-signature support, which makes it easier to satisfy different requirements without added paperwork.

Some compliance tools also allow firms to monitor changes in tax law or financial regulations in real time. This can be a major benefit for multi-jurisdictional firms or those operating in highly-regulated industries where noncompliance penalties are severe.

Automation

Automation reduces manual entry demands and human error by extension, which allows your team to remain focused on more high-value tasks. Workflow automation tools integrate with other accounting software to cut down on repetitive work, like invoice generation or data syncing. Firms can even use these tools to automate client onboarding, engagement letters, or recurring payroll processes to save hours every week.

More advanced automation setups also use conditional logic to trigger actions based on real-time data. For example, a platform might flag overdue invoices and send reminders automatically, or reroute approval requests based on who’s available.

Scalability

A solid tech stack provides firms with the ability to scale operations without overwhelming staff or losing quality. As client bases grow or new services develop, the right tools keep workflows smooth and predictable. For example, cloud-based software makes it easier to add new users, clients, or datasets without limiting performance.

Invoicing, reporting, and compliance can scale with the business instead of becoming bottlenecks. Scalable applications typically offer tiered or modular pricing, which enables firms to access functions as needed.

Maintaining flexibility is key when firms handle seasonal demand, rapid growth, or expansion into new service areas.

AI’s Impact on Accounting Software

AI has changed the landscape of accounting software dramatically by evolving static data entry tools into intelligent systems. These programs can analyze financial patterns, detect anomalies, and create real-time insights. For example, AI platforms can flag potential fraud or alert accountants to inconsistencies across large datasets.

In bookkeeping, AI tools point out trends from historical data to categorize transactions more accurately over time, which minimizes the need for human input.

Financial forecasting tools can simulate an array of business scenarios (based on real-time numbers and market indicators) to help firms prepare for future risks.

Client advisory services professionals are also adopting AI. Rather than dedicating hours to building reports, firms can develop them immediately to initiate proactive conversations with clients.

Tools to Have in an Accounting Tech Stack

A comprehensive accounting tech stack includes, but isn’t limited to, tools for core bookkeeping, document management, CRM, security, time tracking, tax preparation, and payment processing.

Firms should also consider platforms for internal communication and knowledge sharing, especially in remote or hybrid teams.

Accounting / Bookkeeping Tools

Bookkeeping and financial reporting tools are core components of an accounting firm's tech stack. Tools like QuickBooks and Xero make it easier to manage ledgers, reconcile accounts, and produce financial statements. Their cloud-based systems also enable teams to contribute to projects from anywhere.

These platforms also integrate with dozens of other apps to ensure functionality without requiring new workflows. Some provide dashboards clients can use to check real-time metrics, which adds a layer of convenience and transparency.

For firms in niche industries, specialized tools like FreshBooks for freelancers or Wave for micro-businesses may also be useful. These tools offer basic accounting, and some provide invoicing, project tracking, or expense categorization.

Project Management Tools

Project management software helps accounting firms stay organized, meet deadlines, and make sure team members understand their responsibilities. These tools simplify assigning tasks, setting due dates, tracking progress, and allocating resources.

Asana and Trello are popular options due to their visual task boards and ease of use. Other options, like Monday or ClickUp, offer users Gantt charts and time tracking tools.

For accounting firms with various concurrent projects, these platforms can improve visibility into workload and prevent bottlenecks. They're also a central hub for documentation, communication, and updates, which greatly reduces the need for back-and-forth emails.

Marketing Tools

Marketing tools empower firms to build brand recognition, increase client loyalty, and grow their base through digital outreach. Try one or more of the following for better marketing campaigns.

These platforms support functions like automated email campaigns, landing page creation, audience segmentation, social media scheduling, and performance tracking.

- HubSpot, for example, offers full-funnel marketing automation, which makes it ideal for firms that want to nurture leads over time.

- Mailchimp is known for ease of use and powerful analytics, helping teams understand what content drives engagement.

- Tools like Hootsuite allow you to monitor multiple social media platforms in one dashboard, which streamlines your outreach across LinkedIn, Twitter, Facebook, and more.

Security Software

Perhaps one of the most important components of any tech stack, security software protects client data and meets cybersecurity compliance requirements. Consider these tools:

- 1Password or LastPass for password management

- Duo Security or Okta for identity management

- CrowdStrike or SentinelOne for endpoint protection

Cyber insurance providers often require basic tools like MFA and device encryption before issuing policies, which makes these both a smart and essential move.

Security measures also build trust with clients. By showcasing your firm’s commitment to safeguarding sensitive financial information, you promote professionalism and reduce the risk of breaches or reputational harm.

With growing concerns about phishing attacks and ransomware, proactive security is now a baseline expectation. Further, tools like Duo and Okta help manage secure logins across multiple platforms in an effort to make it easier for teams to adopt security best practices without adding friction.

Tax Planning Tools

Tax planning and preparation can be complicated, whether that's due to the long, tedious work involved or the constantly changing tax landscape. It's wise to make sure your tech stack has a dedicated tax planning tool that handles preparation, planning, and filing.Some tax tools include:

- Drake Tax

- CCH Axcess

- Tax ProConnect

- TaxDome

Many of these platforms also provide collaborative access so clients can upload documentation and e-sign forms securely.

In addition to saving time, these tools help minimize human error, ensure compliance with the latest tax codes, and accelerate filing times. Most offer audit trails and secure file sharing, and some include AI-powered diagnostics to flag inconsistencies or missing data. Integrating your tax software with your document management system can also enhance efficiency, especially for high-volume firms with multiple preparers.

AI-Driven Tools

While AI is not a replacement for dedicated human effort, these tools can make time management and productivity more accessible. AI programs can take a lot of the manual requirements out of overseeing financial operations.

Boost your firm's productivity and insights with AI-powered solutions like:

- Vic.ai for invoice automation

- Botkeeper for bookkeeping

- Data rails for financial planning and analysis

- Planful for AI-driven reporting

What sets AI-driven tools apart is their ability to learn from your firm’s data over time. Instead of automating one task, they continuously improve processes.

Payment Processing Tools

Introducing specific tools can make it a lot easier for clients to pay invoices and for the firm to keep track of revenue. To streamline payment processing and revenue monitoring, consider the following tools:

- Stripe

- Square

- PayPal

- Bill.com

- Melio

Integrated payment tools also reduce errors and speed up receivables, which often trigger automatic reconciliations in your accounting software.

For example, when a client pays through Stripe or Melio, that transaction data can be synced directly to your accounting platform. This eliminates manual entry, decreases the chance for mismatched records, and helps ensure your books reflect real-time cash flow. Automatic reconciliations mean your team spends less time matching payments with invoices and more time delivering value-added services.

These tools also improve the client experience. Allowing customers to pay online with a credit card or ACH transfer makes it easier for them to follow through, which can reduce average payment times and improve your cash position. Some tools even support recurring billing, payment reminders, or mobile-friendly options.

Time Tracking Tools

Tracking billable hours leads to more accurate invoicing and improves resource planning. A few reputable time tracking applications include:

- Toggl Track

- Harvest

- Clockify

- QuickBooks Time

Linking time tracking tools with your project management system can also help managers assess efficiency and predict future capacity. These tools are especially valuable in firms where accurate billing is essential for revenue recognition, such as in client-based billing models or time-and-materials engagements.

In addition to tracking time, many time tracking tools offer built-in project management features that allow for better team coordination. For example, some platforms offer integrations with task management systems to enable firms to track how much time is being spent on specific deliverables. This helps identify whether any tasks are consistently taking more time than expected.

With time tracking tools, firms can also gain a more granular view of team productivity by analyzing data (ex: time spent per client, per project, or per team member). This helps firm leaders identify which projects or clients are more time-intensive and whether the current resources are adequate to meet deadlines. Some tools also allow firms to categorize time entries by activity type, which can further aid in decision-making and improve operational transparency.

HR and Payroll Software

Finally, handling employee onboarding, payroll, and benefits can be more easily managed with programs like:

- Gusto

- Rippling

- BambooHR

- ADP

- Zenefits

Many of these tools also handle compliance with labor laws and generate tax documentation automatically.

These platforms streamline hiring, document management, time-off tracking, and benefits enrollment. They also help ensure compliance with changing state and federal employment regulations.

Additionally, cloud-based HR platforms often integrate with your accounting and time tracking systems, giving you a 360-degree view of workforce-related expenses. This is especially useful for budgeting and forecasting. For multi-office or remote firms, centralized HR software ensures consistency in onboarding and record-keeping, no matter where your team is located.

What to Consider When Building an Accounting Tech Stack

When evaluating software options, consider these factors to make sure you're developing a stack that works for you and your firm, not against you. Don’t rush this process. Each tool you add should solve a problem, integrate well, and be easy to use.

Goals

Before choosing any new tool, define your firm’s goals. Are you looking to reduce turnaround times, increase billable hours, simplify client communications, or address compliance risks? Each of these objectives will point to different tools within your tech stack.

For example, a goal to boost productivity might lead your team to invest in workflow automation software. A goal to enhance client retention, on the other hand, could call for a better CRM system.

Clearly defined goals prevent software bloat by ensuring each addition serves a measurable purpose. This also makes it easier to determine ROI after implementation. Write down your team's top three goals and use them as a filter for tech decisions. If a tool doesn’t support at least one, it's likely not the right fit.

Pricing

Cost is always a factor, but it shouldn't be the main factor. Cost should be weighed against the time savings and long-term value a tool provides. When evaluating pricing, consider onboarding fees, training costs, and potential custom integration needs, not just the subscription cost.

It's also important to factor in the cost of inaction. Manual processes and inefficient workflows can cost a great deal more in lost time and productivity than a reasonably priced tool. A carefully structured budget should support your firm's growth goals and focus on tools that have a clear ROI.

Many platforms follow a tiered pricing model, so users can start with a basic plan and upgrade as the company's needs grow.

User Reviews

User reviews are a helpful resource when exploring new software. Sites like G2, Capterra, and TrustRadius showcase verified reviews of users' real-world experiences. Look for patterns in the feedback.

For example, several mentions of poor customer service or frequent bugs should be a red flag. Consistent praise for ease of use or quick implementation is a good sign.

Don’t review star-only ratings. Read detailed comments to gather context. Reviews are also a great tool for narrowing down similarly priced options. If a tool has relatively positive ratings, an active user community, and regular updates, it indicates reliability.

Integrations

Effective integrations remove data silos, reduce manual data transfers, and unlock automation opportunities. An effective tool should integrate smoothly with your existing tech stack, including your accounting software, CRM, payroll system, and project management apps. Before committing, review the integration options listed on the vendor’s website.

Some platforms offer native integrations, others use APIs or third-party services like Zapier to connect with other tools. Focus on tools with pre-built integrations that support real-time data syncing. Avoid solutions that need custom coding unless you have dedicated IT resources.

Ease of Use

Even the best software won't help your accounting firm if your team finds it difficult to use. When reviewing your options, look for intuitive design, easy navigation, and a minimal learning curve. Platforms that are user-friendly save time and money when it comes to onboarding and training. Seek out vendors that offer tutorials and built-in support features (like guided walkthroughs).

A well-designed interface leads to quicker adoption, reduces user errors, and increases the odds of employees using the tool long-term. During demos or trial periods, be aware of how team members interact with the platform. Do they understand how to complete basic tasks without help? Do they feel confident using the tool after basic instruction?

Customer Support

Responsive and knowledgeable customer support can make or break your experience with a tool. When issues arise, you need assurance that help will be available right away. Look for platforms that offer a selection of support channels, such as live chat, phone, email, or dedicated account managers. Some vendors also have curated knowledge bases on their websites, including guides, training videos, and user communities.

Check support hours to make sure they align with your company's schedule, especially if your firm works outside standard hours.

Onboarding

Onboarding is an often overlooked part of adopting new tools. A smooth onboarding experience helps teams increase their productivity faster and improves the likelihood of success with the platform. Ask potential vendors about their onboarding process. Do they provide setup assistance, data migration support, or specialized training? Do they assign a customer success manager to guide your firm through the early stages?

Firms should also create internal onboarding checklists to ensure team members can use new tools effectively. A good onboarding process can also reveal opportunities for workflow improvement that weren’t obvious during the sales process.

Best Practices for Choosing the Right Tech Stack

Building a future-proof accounting firm tech stack requires a carefully formulated strategy. Here are a few tips to guide your selection and optimization process.

- Identify pain points

- Prioritize integrations

- Document workflows

- Eliminate unnecessary steps

- Focus on user adoption

- Involve your team

Start by identifying your firm’s pain points. For example, are you wasting time on manual data entry? Struggling to manage client communications? Constantly chasing down invoices? Each issue points to a category of tools that could help. From there, prioritize integrations. Tools that work well together reduce redundancies and unlock more effective automation efforts.

As you evaluate tools, take the time to document current workflows and note any bottlenecks or duplicated efforts. This baseline will help you measure improvements after implementation. You may also uncover processes that can be entirely eliminated with the right tool. And the right tool saves time, reduces training needs, and improves staff morale by removing frustration from daily tasks.

Also, consider user adoption. The best tools in the world are useless if your team doesn’t use them. Schedule demos, involve team members in the evaluation process, and focus on platforms with clean, intuitive interfaces. Where possible, take advantage of free trials or sandbox environments before you commit.

Make Your Accounting Tech Stack Work Smarter with Zylo

An optimized accounting tech stack automates tasks, improves client service, and supports growth. But without visibility into software usage and renewals, stacks can become bloated. That’s why firms are adopting strategic SaaS Management, which is often led by ops or finance.

Tools like Zylo for Software Asset Managers provide firmwide visibility, helping reduce costs, streamline procurement, and refine tech strategy.

SaaS Management cuts waste from unused licenses and duplicate tools, improve forecasting, and enablie smarter planning for renewals, upgrades, and training.

To go deeper, explore the 2026 SaaS Management Index for the latest data and benchmarks across industries.